What is Balance Sheet: Its Use and Importance

Balance sheet is a type of financial statement that provides data related to a company’s assets, liabilities, and shareholder’s equity. Through a balance sheet, you can also identify investments by shareholders.

In this article, we will be discussing Balance sheet that helps in understanding the company’s financial status in detail.

Table of Contents

- What is balance sheet?

- Why do we need it?

- Guidelines Followed

- Format

- Analysis

- Components

- Limitations

What is Balance Sheet?

This financial statement is used for fundamental analysis to evaluate the financial health of a business. Experts can use balance sheets for calculating financial ratios as well. It is prepared and shared as per the frequency of reporting determined by the company. It may be distributed on a quarterly or on monthly basis. This is a financial statement that provides the financial summary of any business. Its purpose varies on the basis of the type of review. Let us understand how the need for a balance sheet.

Why Do We Need a Balance Sheet?

When the balance sheet is reviewed internally, it provides insight into the success and failure of a company. When it is reviewed externally, it provides insight into the available resources’ success. It also indicates the way in which they are financed.

Through the sheet, businesses and investors can equally benefit in the following manner:

- Businesses can identify areas of improvement so that their finances keep on thriving.

- Investors can decide whether a company is worth investing money or not.

- Auditors can assess whether the company is in compliance with reporting guidelines and laws.

- Organizations can calculate important financial metrics, including liquidity, debt-to-equity ratio, and profitability.

Guidelines Followed

Balance sheets are mostly based on either of the two accounting guidelines: GAAP or IFRS. If your firm is in the U.S., you will have to create a balance sheet based on the GAAP guidelines. If your business is outside the U.S., then in most cases, you will follow IFRS guidelines.

In case, you are creating a GAAP-based sheet. In such a case, the company assets should be listed in the descending order of their liquidity. High liquidity assets are above low liquidity assets. Also, current assets are placed above non-current assets.

Explore GAAP courses

The IFRS-based balance sheet reports assets in the increasing order of their liquidity. Assets with lower liquidity will be placed above assets with higher liquidity. That means non-current assets will be placed before current assets on the balance sheet.

Check out IFRS online courses

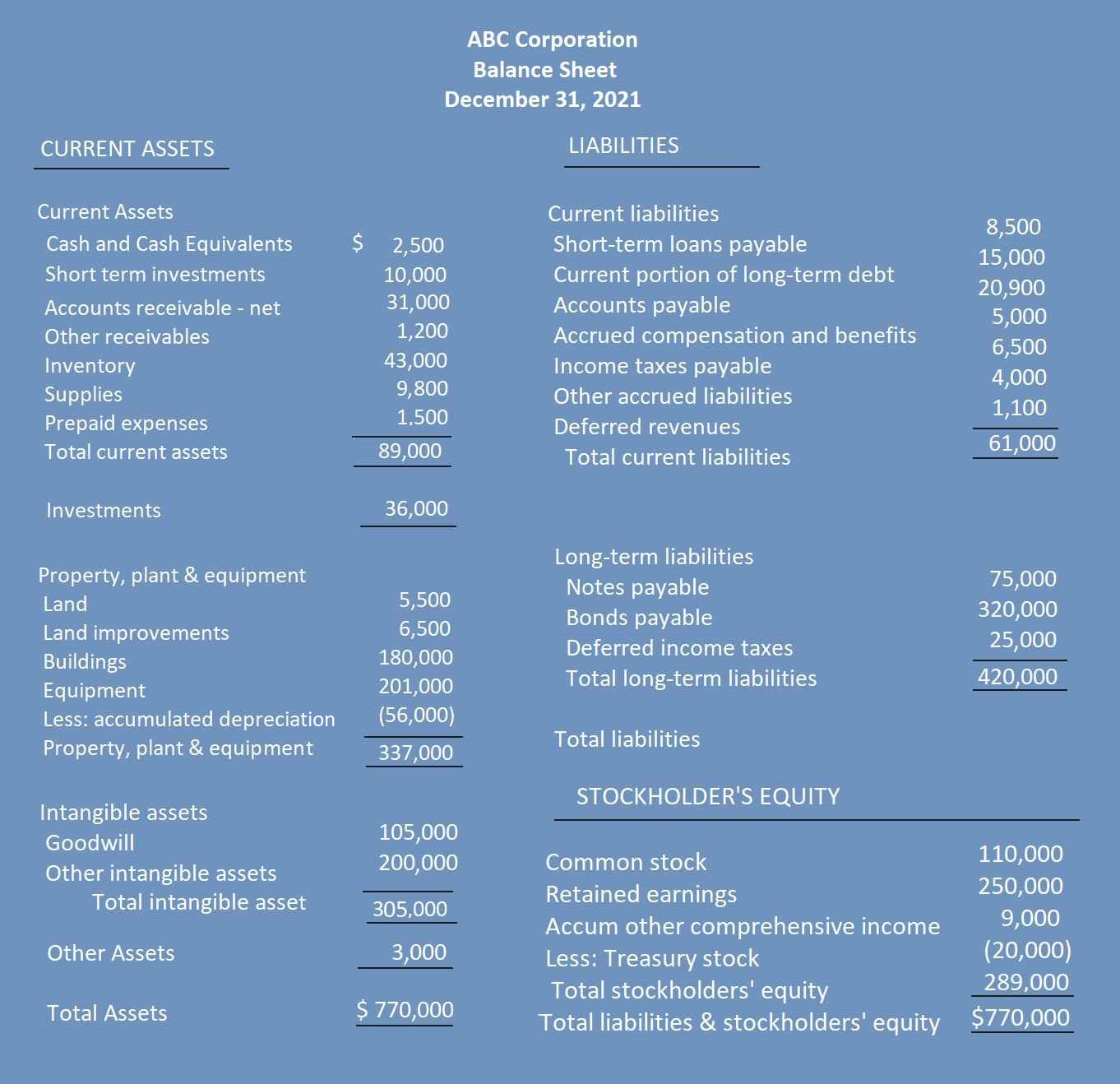

Balance Sheet Format

Let us now go through the balance sheet in detail. Here, we are considering one of the sample balance sheet templates. The sheet is broadly divided into assets and liabilities. At the top, assets are listed and liabilities are listed at the bottom. The assets should be organized in order of their liquidity.

The order should be descending. This means that the higher liquidity assets should be on top whereas low liquidity assets should be placed below that. In the case of liabilities, the accounts are organized from short-term to long-term obligations. The final requirement from the sheet is that the total assets should be equal to total liabilities. Then only, the sheet will be in balance.

Analyzing a Balance Sheet

To analyze the balance sheet, an analysis of financial ratios is also conducted by experts. Through the balance sheet, four main ratios can be determined. These include activity ratios, debt-to-equity, working capital, and financial strength ratios.

Through this analysis, experts can assess the operational efficiency of a company. They also help experts understand the company’s ability to meet its obligation and how it leverages them. Through in-depth analysis, investors can assess how the company finances itself and also if it is financially stable.

Read Later

Read Later

Components

A balance sheet is composed of three components that are mentioned in its equation as well:

Assets = Liabilities + Shareholder’s Equity

Let us learn about these components in detail in the following section.

1. Assets

As already mentioned, assets are listed in descending order of their liquidity. This means that more liquid assets are listed above less liquid assets. Assets include current and non-current assets.

- Current assets are very easily converted into cash within a period of one year. These are short-term assets. Cash equivalents, cash, and marketable securities, inventory, accounts receivable, and prepaid expenses are current assets.

- Non-current assets cannot be liquidated within the period of one year. They need more time and are long-term assets. These include intangible assets, fixed assets, and long-term investments.

2. Liabilities

These refer to the money that companies owe to external parties. Liabilities include interest, bills, rent, and salaries. There are current liabilities and long-term liabilities.

- Current liabilities need to be paid within the time period of one year. Salary, wages, interest, earned and unearned premiums, customer prepayments, dividends, and accounts payable are current liabilities.

- Long-term liabilities are long-term debts. These include pension fund liabilities, interest and principal on issued bonds, and deferred tax liabilities.

3. Shareholder Equity

Equity refers to the shareholder money that the company owes. It is the difference between total assets and liabilities. It includes controlling interest and non-controlling interest.

- Controlling interest: These include reserves and issued capital that are attributable to equity holders of the parent company.

- Non-controlling interest in equity.

It can be calculated through the following equation:

Shareholders’ Equity = (Retained Earnings + Company’s share capital) – Value of treasury shares

Check out accounting courses

Limitations

A balance sheet does have certain limitations. Unlike the income statement, it is static in nature. Due to this, all three financial statements are required for a complete understanding of the company’s financial situation.

Balance sheets are significant at a specific point in time; you will require the past sheet to utilize the current one. Moreover, different accounting systems impact the figures on a balance sheet.

Conclusion

A balance sheet is very significant for every business. However, its use is incomplete without income statements and the statement of cash flows. All these together provide the complete financial situation of the company. This makes the understanding of each one mandatory for a complete financial analysis of the company.

FAQs

What are the common types of the balance sheet?

The common size, comparative, vertical, and classified balance sheets are commonly used.

What are the different parts of a balance sheet?

A balance sheet consists of assets ( current, non-current, and total assets). It also includes equity and liabilities (current and non-current liabilities).

What is the formula used in a balance sheet?

A balance sheet works on the formula of balancing assets and liabilities. 'Assets = Liabilities + Equity' is the equation used in a balance sheet.

What are the different methods of classifying an asset?

Physical existence, convertibility, and usage are the three methods of classifying assets.

Is rent payable liability or an asset?

Rent payable falls under the liability account in the general ledger.