Solvency Ratio: Formula, Interpretation, Examples, Tips to Improve it

The solvency ratio is a fundamental indicator of any company’s financial health. Its calculation and analysis let us know if an entity can solvently pay all its commitments or debts. The solvency ratio helps stakeholders, including investors, leaders, and shareholders, evaluate the company’s financial health and capacity to remain profitable over an extended period.

What is Solvency Ratio?

The solvency ratio is a financial metric that assesses a company’s ability to cover its long-term liabilities.

Solvency ratios prioritize actual cash flow over net income. This approach considers factors such as depreciation and expenses, which impact a company’s ability to generate cash and meet its financial obligations.

Solvency ratios offer a comprehensive view of a company’s financial health and ensure that the analysis accounts for both short-term and long-term debt, providing a more accurate assessment.

- Solvency Ratio Formula

- Example of Solvency Ratio

- How to Interpret the Solvency Ratio?

- Types of Solvency Ratios

- How to Improve the Solvency Ratio?

Best-suited Banking, Finance & Insurance courses for you

Learn Banking, Finance & Insurance with these high-rated online courses

Solvency Ratio Formula

The Solvency Ratio Formula is as follows –

Example of Solvency Ratio

Let us consider a company X which has closed the FY 2022-2023 with the below annual financial data –

- Net Income: Rs. 1,850 crores

- Depreciation: Rs. 235.7 crores

- Short-term debt: Rs. 991 crores

- Long-term debt: Rs. 1,123.5 crores

Solvency Ratio = (Short-term Debt + Long-term Debt) / Equity

Given the financial data, first, we need to calculate the company’s equity. You can calculate equity using the below formula:

Equity = Net Income + Depreciation

Equity = Rs. 1,850 crores + Rs. 235.7 crores = Rs. 2,085.7 crores

Now, we can calculate the solvency ratio:

Solvency Ratio = (Short-term Debt + Long-term Debt) / Equity

Solvency Ratio = (Rs. 991 crores + Rs. 1,123.5 crores) / Rs. 2,085.7 crores

Solvency Ratio ≈ 1.05

In this example, the solvency ratio is approximately 1.05. This means that for every Rs. 1 of equity, the company has Rs. 1.05 of debt (both short-term and long-term combined). A solvency ratio above 1 indicates that the company has more debt than equity, which suggests a higher degree of financial risk.

Read Later

Read Later

How to Interpret the Solvency Ratio?

When interpreting the solvency ratio, it’s important to consider industry benchmarks and the company’s specific circumstances. A higher ratio may indicate a higher level of financial leverage, which can be acceptable or risky depending on the industry and the company’s ability to service its debt obligations.

Here’s a detailed interpretation of the solvency ratio:

- Solvency Ratio Less Than 1: The solvency ratio of less than 1 indicates that the company’s total debt exceeds its equity. In these circumstances, the company may be technically insolvent, meaning it doesn’t have enough assets to cover its obligations. The solvency ratio of less than 1 is a red flag suggesting financial distress or bankruptcy.

- Solvency Ratio Equal to 1: A solvency ratio of 1 means that the company’s total debt equals its total equity. While this technically implies a balance between debt and equity, it doesn’t indicate the business’s financial health is excellent. It is a borderline situation, and the company might struggle to cover its debt obligations.

- Solvency Ratio Greater Than 1: A solvency ratio above 1 suggests that the company has more equity than debt. This is generally a positive sign. It indicates that the company has the financial resources to cover its debt obligations. A solvency ratio above 1.5 indicates good financial health because it provides a comfortable buffer to meet obligations.

- Solvency Ratio Significantly Greater Than 1: A significant solvency ratio above 1 may indicate that the company has good equity and a higher growth potential or returns value to shareholders through dividends or share buybacks.

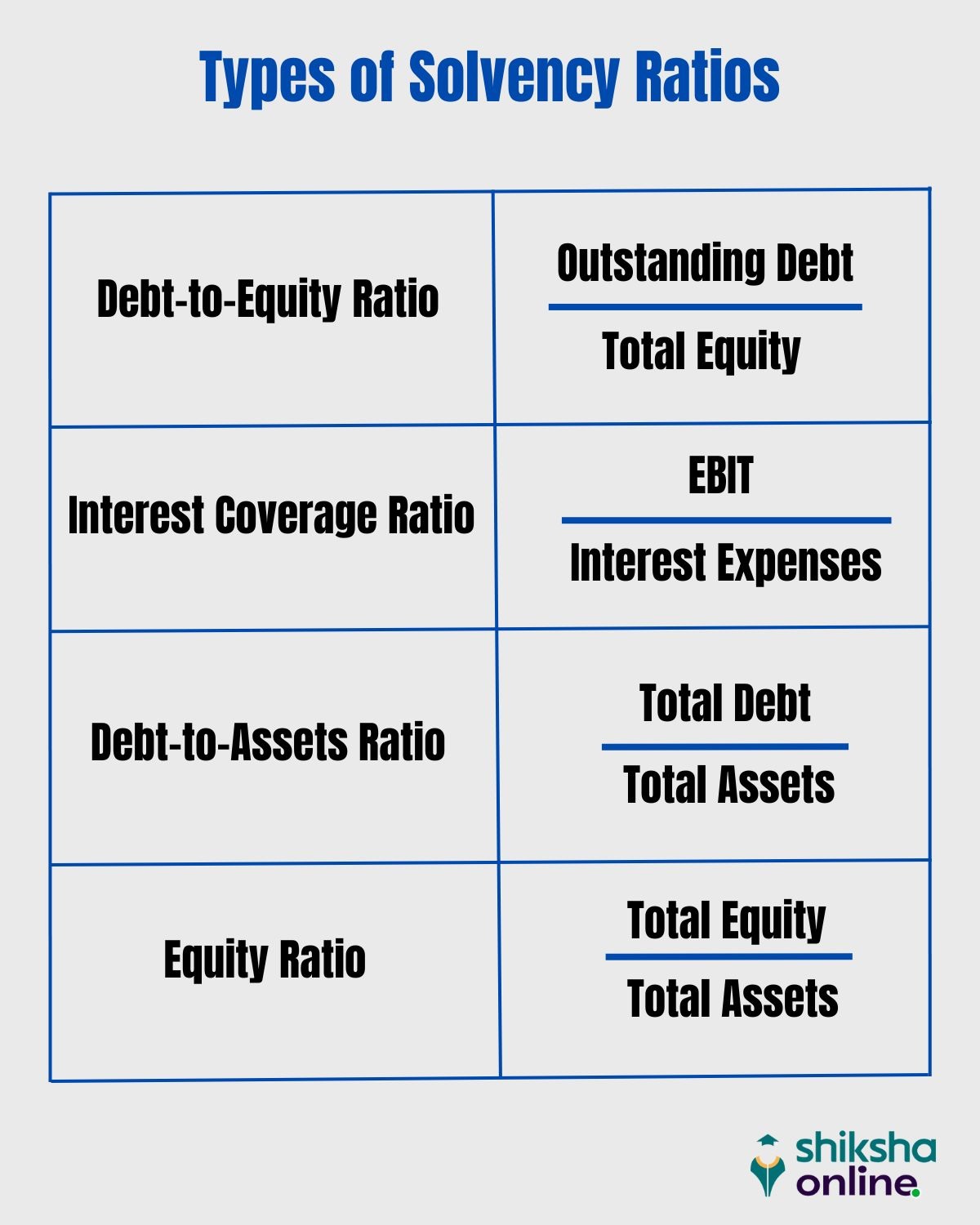

Types of Solvency Ratios

There are four types of solvency ratios –

Debt to Equity Ratio

The Debt to Equity Ratio measures the proportion of a company’s total debt to its total equity. It indicates how much a company relies on debt financing versus equity financing.

A lower ratio suggests lower financial risk, while a higher ratio may indicate higher financial leverage.

Debt to Equity Ratio = Total Debt / Total Equity

Example –

To calculate the Debt-to-Equity (D/E) Ratio, let’s take the example of a fictional company, Company A. Here’s the financial data for Company A, where –

Total debt: Rs. 2,500,000

Total equity: Rs. 5,000,000

Using the provided data:

=> Rs. 2,500,000 /Rs. 5,000,000 = 0.5

So, the Debt-to-Equity Ratio for Company A is 0.5.

Interpretation: A Debt-to-Equity Ratio of 0.5 indicates that Company A has ₹0.5 in debt for every ₹1 in equity. This ratio suggests that the company has a moderate level of debt relative to its equity, and its financial position can be considered balanced. It’s neither excessively leveraged nor highly equity-funded.

Must Read – Difference Between Debt and Equity

Interest Coverage Ratio

The Interest Coverage Ratio is also known as the Times Interest Earned (TIE) ratio. It measures a company’s ability to cover its interest expenses with earnings before interest and taxes (EBIT).

A higher interest coverage ratio indicates a lower risk of defaulting on interest payments.

Interest Coverage Ratio = EBIT / Interest Expenses

Example –

Here’s the financial data for Company B:

Operating income: Rs. 10,00,000

Interest expense: Rs. 2,50,000

Now, let’s calculate the Interest Coverage Ratio:

=> Rs. 10,00,000 / Rs. 2,50,000 = 4

So, the Interest Coverage Ratio for Company A is 4.

Interpretation: An Interest Coverage Ratio of 4 indicates that Company A generates four times the operating income needed to cover its interest expenses. In other words, the company’s operating income is sufficient to cover its interest payments comfortably. A higher Interest Coverage Ratio implies a lower risk of defaulting on debt obligations.

Debt-to-Assets Ratio

The Debt-to-Assets Ratio measures the proportion of a company’s total assets financed by debt. It provides a snapshot of the company’s financial leverage and risk. A higher ratio indicates a larger portion of debt-financed assets, which can increase financial risk if the company cannot meet its debt obligations.

Debt-to-Assets Ratio = Total Debt / Total Assets

Example –

As an example, we will take the financial data for Company C:

Total debt: Rs. 3,00,000

Total Assets: Rs. 8,00,000

Now, let’s calculate the Debt-to-Assets Ratio:

=> Rs. 3,00,000/Rs. 8,00,000 = 0.375

So, the Debt-to-Assets Ratio for Company A is 0.375.

Interpretation: A Debt-to-Assets Ratio of 0.375 (or 37.5%) indicates that 37.5% of Company A’s total assets are financed by debt. In other words, for every Rs. 1 of assets, the company has Rs. 0.375 in debt. A lower Debt-to-Assets Ratio suggests that a larger proportion of the company’s assets are financed by equity, and the company’s position can be considered conservative or financially cautious.

Equity Ratio

The Equity Ratio, also known as the Equity-to-Assets Ratio, assesses the portion of a company’s total assets financed by equity. It provides insight into the company’s financial stability and the extent to which shareholders have a claim on the assets.

A higher equity ratio indicates a larger portion of equity-financed assets, generally seen as a positive sign of financial strength.

Equity Ratio = Total Equity / Total Assets

Let’s calculate the Equity Ratio of Company D using hypothetical financial data.

Total Equity: Rs. 800 crore

Total Assets: Rs. 1,200 crore

Equity Ratio = Rs. 800 crore / Rs. 1,200 crore

Equity Ratio = 2/3 or ~0.67

Interpretation: So, Company D has an Equity Ratio of ~0.67, which means that 67% of its total assets are financed by equity, while the remaining 33% is financed by debt. This suggests that Company D relies more on equity financing to support its operations and investments, indicating a relatively stable and less leveraged financial structure.

How to Improve the Solvency Ratio?

When you get this far, you should be eager to take actions that optimize your company’s solvency.

Consider applying the following advice to minimize the probability of default as well as bankruptcy –

Find Ways To Earn Extra Money

The more you earn, the better economic situation you will have. Innovate and bring in different approaches to increase sales, create new products or services, and invest in assets that generate profits passively without having to dedicate so much time.

Save at least 10% of Business Income.

Plan your business move strategically. Saving money will allow you to build a cushion to face unforeseen events and times of crisis. Or, more importantly, to invest in business expansion or the creation of new products and services.

Simplify Processes

When workflows are simpler, you invest less time and resources, spending less money on operations.

Adopting technologies is a good way to simplify them. Accounting software, for example, can significantly reduce work in this area, helping you optimize results and giving the accountant time to address more important issues, such as financial, tax and legal analysis.

Buy Smart

Evaluate your options well. Enquire about all sorts of solutions available in the market and analyze their cost-benefit. Make every purchase rationally and, preferably, consult the accountant’s opinion before concluding a deal.

Manage Working Capital

Efficient working capital management, such as optimizing inventory levels, reducing accounts receivable collection periods, and extending accounts payable, can free up cash to reduce debt or increase equity.

Refinance Debt

Explore opportunities to refinance debt at lower interest rates or more favourable terms. This can reduce interest expenses and make debt servicing more manageable.

Diversify Revenue Streams

Reducing dependency on a single product, customer, or market can mitigate risks and improve long-term profitability, indirectly enhancing the solvency ratio.

Conclusion

Solvency ratios are essential for evaluating a company's long-term financial viability and ability to fulfil its financial commitments. Solvency ratios should be used with other financial metrics, such as liquidity and profitability ratios, to comprehensively understand a company's financial health. By understanding and interpreting these ratios effectively, investors, creditors, and company management can make informed decisions that contribute to the company's long-term success.

FAQs

What does a high solvency ratio indicate?

A high solvency ratio suggests a lower financial risk, meaning the company has more equity to cover its long-term debts.

What are the key components of the solvency ratio calculation of a company?

The key components of the solvency ratio calculation of a company are total debt, total equity, and sometimes total assets, depending on the specific ratio being used.

Can a company with a low solvency ratio secure financing or credit?

Companies with low solvency ratios may face challenges in securing financing, and creditors may view them as riskier borrowers, potentially leading to higher borrowing costs.

What are some red flags in solvency ratios to watch out for?

Red flags may include solvency ratios significantly below 1, indicating a high level of debt relative to equity, and deteriorating ratios over time, which may signal financial distress.

Rashmi is a postgraduate in Biotechnology with a flair for research-oriented work and has an experience of over 13 years in content creation and social media handling. She has a diversified writing portfolio and aim... Read Full Bio