Trial Balance – Definition, Features, Benefits, Errors, Example

The goal of every business is to be profitable. You must keep track of market movements and your numbers to achieve this. Accounting is the primary tool to keep a detailed record of economic movements so that the entrepreneur can know the actual financial situation of the business, be aware of the profits and losses, and know its solvency to plan the strategy for the future. The trial balance of sums and balances is an essential piece of accounting. Let’s learn about it in the article.

Content

- What is Trial Balance?

- Content of the Trial Balance

- Features of a Trial Balance

- Advantages of Generating Trial Balance

- How is the balance of sums and balances made?

- Errors Affecting the Trial Balance

- Errors That Do Not Affect The Trial Balance

What is Trial Balance?

The trial balance is an accounting instrument used to establish a summary of the financial status, and operations carried out in the company during a determined period. It reflects the sum of the debits and credits of the different accounts and their corresponding balance.

This accounting instrument verifies that all the balances we use during the fiscal year are reliable.

Read Later

Read Later

Best-suited Banking, Finance & Insurance courses for you

Learn Banking, Finance & Insurance with these high-rated online courses

Content of the Trial Balance

Every trial balance must contain the following:

- Name of the business (company name)

- Specifications

- Time period

- Account code

- Account name

- Total debit and credit balance of the accounts

Features of a Trial Balance

- It is the transition point between the recording system and accounting theory. Financial information is provided to prepare and submit a worksheet through such a statement.

- Includes transactions recorded on a cash basis and accrual basis.

- It is prepared and presented periodically, subject to current accounting standards. The periodicity, both from the technical and legal point of view, is annual. However, it is recommended that a company’s preparation and presentation be monthly for internal use.

- It does not include a column for the date because it is prepared periodically.

- Displays accounts and balances provided by ledger records.

Explore GAAP courses

Advantages of Generating Trial Balance

For accountants who prepare financial reports, trial balance –

- Allows establishing the period’s movements, observing compliance with recognition principles, initial and subsequent measurement, and derecognition.

- Allows you to analyze the balances of the items that make up an account to express whether your balance is adequate.

- Enables determining materiality and relative importance criteria in the financial statements.

- Allows for determining errors in account balances (items with a sign contrary to their nature).

- Checks the double entry that the sum of the debits equals the credits.

- It makes it possible to identify whether accounting estimates have been made on any items in the statement of financial position and the statement of comprehensive income.

Explore IFRS courses

For the tax auditor –

- Verify the adequacy of the journal entries recorded in the general ledger and other adjustments made to prepare the financial statements.

- Verify the balances of the trial balance with the financial statements that will be subject to an opinion.

- Perform audit procedures to verify assertions.

- Application of analytical review procedures.

- Identification of significant management accounts and assertions.

- Identification of control procedures.

Check out accounting courses

How is the balance of sums and balances made?

The trial balance must contain

- The business name

- The identification of the state to which it refers

- The period or date in which it is made

Must Read –What is Finance?

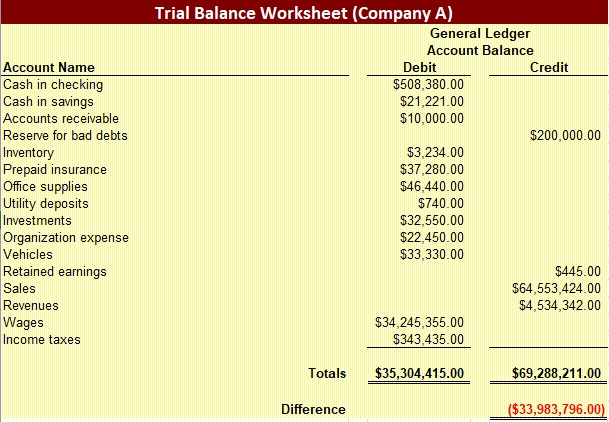

Here is an example of the Trial Balance of Company A.

The company’s Trial Balance shows that the credit amount is higher than the debit, showing that Company A is profitable.

How To Create a Trial Balance?

To prepare a trial balance accurately, it is essential to follow a structured approach:

- Record all financial transactions in the Daily Book, ensuring every entry is posted to the corresponding account in the General Ledger.

- Calculate the total debits and credits separately for each account by adding up the respective amounts.

- Determine the balance of each account by subtracting the credit total from the debit total. This will result in either a debit balance (if debits exceed credits) or a credit balance (if credits exceed debits).

- Create a table with one account per row. The columns should display the sum of all debits, the sum of all credits, credit balances, and debit balances.

- In the last two columns, indicate the account balance amount based on whether it represents a debtor (if it has a debit balance) or a creditor (if it has a credit balance).

- Validate your trial balance by summing up each column's rows to ensure that the total debits match the total credits, confirming that your accounting records are balanced.

Errors Affecting the Trial Balance

Trial balances do not balance because of an error in entries or a mistake in the initial calculations. Therefore, you must carefully review the journal entries, looking for discrepancies.

Some of the most common accounting errors are omitting or repeating a number or account, mistakenly writing down an item that does not correspond or an error in the dates that makes an operation posted before or after what is due.

The following are examples of errors that affect it:

Errors where partial information has been registered: This can happen when registering an entry in a single account by accident. For example, a debit may be posted for $200, but a credit of $200 was not posted.

Transpose errors where digits may have been changed: In this case, you wanted to record a transaction for $3,900 but recorded debit as $9,300 and credit as $3,900.

General Posting Errors: This includes posting the wrong amount on the wrong side of an account, the correct amount on the wrong side, the correct amount on the right side of the wrong account, etc.

Carryover errors: This is when the error is carried over from one page total to another.

Errors That Do Not Affect The Trial Balance

If you have an error in your trial balance, it will not be one of the following:

- Error of principle in accounting

- Error of omission in accounting

- Commission error

- Compensatory mistake

- Original input error

FAQs - Trial Balance

What is the significance of the trial balance in financial reporting?

The trial balance is a fundamental step in the financial reporting process. It provides the basis for creating financial statements like income and balance sheets.

How is a trial balance prepared?

To prepare a trial balance, you list all the account names and their balances from the general ledger. The debit and credit balances are summed separately and verify that they are equal.

What does it mean if the trial balance balances?

If the trial balance balances, the total debits equal the total credits in the ledger, suggesting that the accounting entries have been recorded accurately.

What should a company do if the trial balance does not balance?

If the trial balance does not balance, it indicates an error in the accounting records. The company should review its transactions and ledger entries to identify and correct the mistake.

Can a trial balance identify all types of errors in accounting records?

No, a trial balance can identify arithmetic errors and some common recording mistakes but may not catch more complex errors, such as omitted transactions or misclassification of accounts.

Rashmi is a postgraduate in Biotechnology with a flair for research-oriented work and has an experience of over 13 years in content creation and social media handling. She has a diversified writing portfolio and aim... Read Full Bio