Transfer Pricing: A Key To Avoid Tax Evasion

Learn about transfer pricing, the art of setting prices between related parties, and how it can help you avoid tax evasion and increase profitability.

Globalization and the digital transformation of industries have caused various changes in the international community at a commercial level to attract capital from other parts of the world. Transfer Pricing is one of the fundamental concepts of this new paradigm that is crucial to know.

In this regard, having the correct knowledge and tools to avoid issues related to Transfer Pricing makes it easier for organizations to meet their demands and benefit from their competitive potential and globalization.

Explore investing courses

What is Transfer Pricing?

Transfer pricing refers to pricing goods, services, or intangible assets exchanged between affiliated companies within the same company.

Transfer pricing becomes necessary to determine whether organizational objectives are being achieved in each company’s department. They are also important in evaluating divisional performance.

Transfer pricing was earlier limited to foreign multinational companies. However, given the increased internationalization of businesses, this concept has become increasingly significant for all companies.

Read Later

Read Later

Best-suited Tax Law courses for you

Learn Tax Law with these high-rated online courses

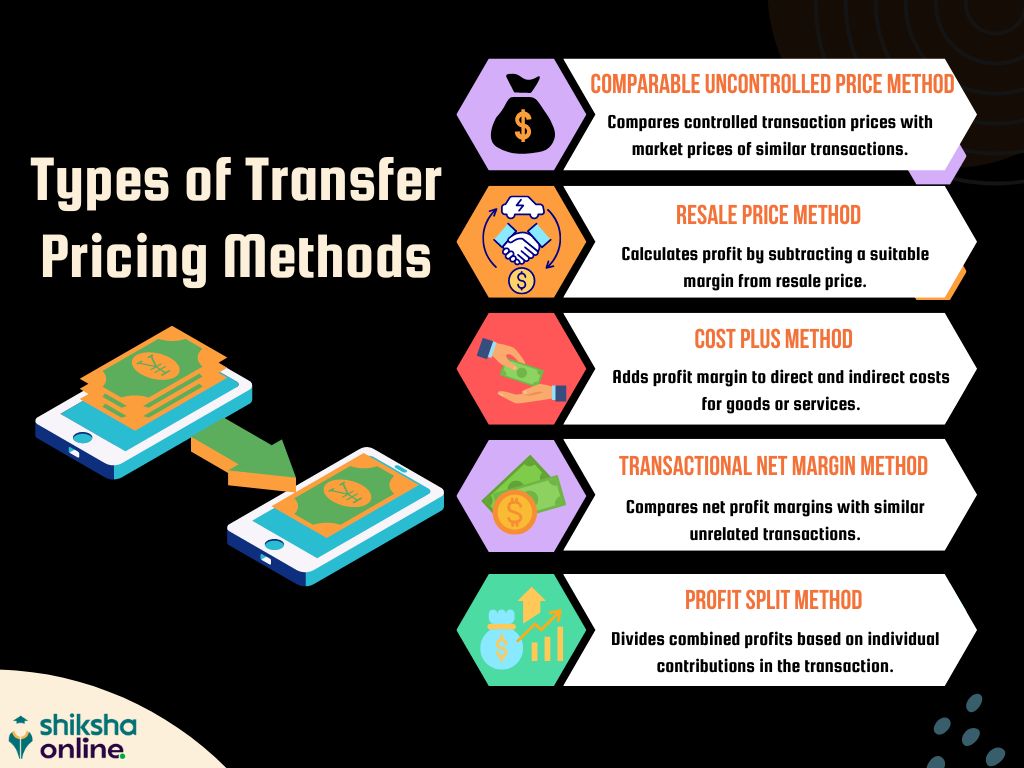

Types of Transfer Pricing Methods

There are mainly 5 types of transfer pricing methods, as follows –

Comparable Uncontrolled Price Method (CUP)

It is the most common and preferred method by the OECD and the tax administrations in most cases. The CUP method compares the price of goods or services in an intercompany transaction with the price exchanged between independent parties.

Goods and services must be valued on comparable terms to obtain an exact price tax administrations will accept. This can also be called set-market pricing because, unlike other methods focusing on margins, the CUP Method is based on a fair market price.

A drawback to this approach is when the external market does not meet the criteria for internal transfer pricing. Commodity prices can be very volatile. For example, prices fluctuate significantly for oil, so for companies that rely on oil for their primary manufacturing activity, the CUP may not be the best transfer pricing model.

Added Cost Method

It is a transaction method that compares gross profit with sales costs. The division supplying goods or services determines the transaction cost and then adds a markup on the goods or services delivered. The profit margin should equal what a third party would earn from transactions in a comparable situation, including similar risks and market conditions.

One drawback is that this method does not necessarily encourage the supply division to be efficient in manufacturing practices. It may be less efficient when limiting things like labour, and avoiding competitive pricing.

Resale Price Method

Analyze the gross margin or the difference between the price at which a product or service is purchased and the price at which it is sold to a third party. Although similar to the CPM, the Resale Price Method only considers the margin (minus associated costs) as the transfer price. For this reason, it is more appropriate for distributors and resellers and not so much for manufacturers.

Transaction Net Margin Method (TNMM)

TNMM recently emerged as the favoured model for many multinationals because the transfer price is based on net profit compared to the comparable foreign market price. The CUP, add-on cost, and resale price methods are based on the actual cost of comparable goods or services for outside transactions. Instead, TNMM compares the net profit margin earned on a controlled intercompany transaction with the net profit margin earned on a similar transaction with a third party.

It compares the profit margin to actual costs. It is especially attractive when external pricing data is unavailable to determine the market price. With TNMM, businesses can measure net profit against sales, costs, or assets. TNMM usually applies by targeting an operating margin within a set range. While tax authorities have preferred the CUP Method, TNMM is emerging as a new standard.

Profit Distribution Method

Like TNMM, it is based on profit, not comparable market price. This method determines the transfer price by evaluating how the profits from a particular transaction would have been divided among the independent companies involved. It is based on the relative contribution of each trading party associated with the transaction.

When Do Transfer Pricing Rules Apply in India?

Here are the scenarios in which transfer pricing rules apply in India:

- International Transactions: Transfer pricing rules apply when an Indian entity enters into a transaction with a non-resident entity. This can include transactions related to the sale, purchase, provision of services, loan transactions, royalty payments, etc.

- Specified Domestic Transactions: Transfer pricing rules also apply to certain domestic transactions that the Income Tax Act specifies. These are transactions between related parties within India, where at least one party enjoys tax benefits under specified provisions.

- Thresholds: When the aggregate value of international or specified domestic transactions during a financial year exceeds a specified monetary threshold. The government determines this threshold, and it is subject to change.

- Exemptions: Small and medium-sized enterprises (SMEs) with total turnover or gross receipts not exceeding a certain threshold may be exempt from transfer pricing documentation requirements, provided certain conditions are met.

- Documentation and Reporting: Taxpayers falling within the scope of transfer pricing regulations must maintain comprehensive documentation. This includes the details of the transactions and any other relevant information as proof of their transactions.

- Advance Pricing Agreement (APA): Taxpayers can enter into an APA with the Indian tax authorities to determine transfer prices in advance. This provides certainty and reduces the risk of disputes.

- Penalties: Failure to comply with transfer pricing regulations can lead to penalties, adjustments to taxable income, and potential disputes with tax authorities.

Key Takeaways

- Transfer pricing is the process of setting prices for transactions between related parties.

- Related parties are businesses under common control, such as parent-subsidiary companies.

- The goal of transfer pricing is to ensure that the prices of transactions between related parties are at arm’s length, meaning that they would be the same if the parties were unrelated.

- Businesses that do not comply with transfer pricing rules may be subject to penalties from tax authorities.

Conclusion

Transfer pricing is a complex and important issue for businesses of all sizes. It is important to understand the basics of transfer prices and how it can affect your business’s tax liability. You should also know the risks of unfair transfer pricing practices and how to protect your business. Understanding transfer prices and taking steps to comply with the law can help ensure your business pays the correct taxes and avoid unnecessary penalties.

FAQs

Who is responsible for transfer pricing?

The responsibility for transfer pricing falls on the businesses involved in the transactions. Businesses need to ensure that they have appropriate transfer pricing policies and procedures in place, and they need to document their transfer pricing calculations.

What are the risks of transfer pricing?

The main risk of transfer pricing is that businesses may use unfair transfer pricing practices to reduce their tax liability. This can lead to penalties from tax authorities.

What are the penalties for non-compliance with transfer pricing rules?

The penalties for non-compliance with transfer pricing rules can be significant. Businesses may be required to pay back taxes, interest, and penalties. They may also be subject to criminal prosecution.

What is the future of transfer pricing?

Transfer pricing is a complex and evolving area of law. Effective transfer pricing compliance will become increasingly important as businesses become more globalized. Tax authorities are also becoming more sophisticated in enforcing transfer pricing rules. This means that businesses need to be aware of the latest transfer pricing developments and take steps to comply with the law.

Rashmi is a postgraduate in Biotechnology with a flair for research-oriented work and has an experience of over 13 years in content creation and social media handling. She has a diversified writing portfolio and aim... Read Full Bio